European government bond dynamics and stability policies: taming contagion risks

Dynamic correlation networks of European sovereign bonds

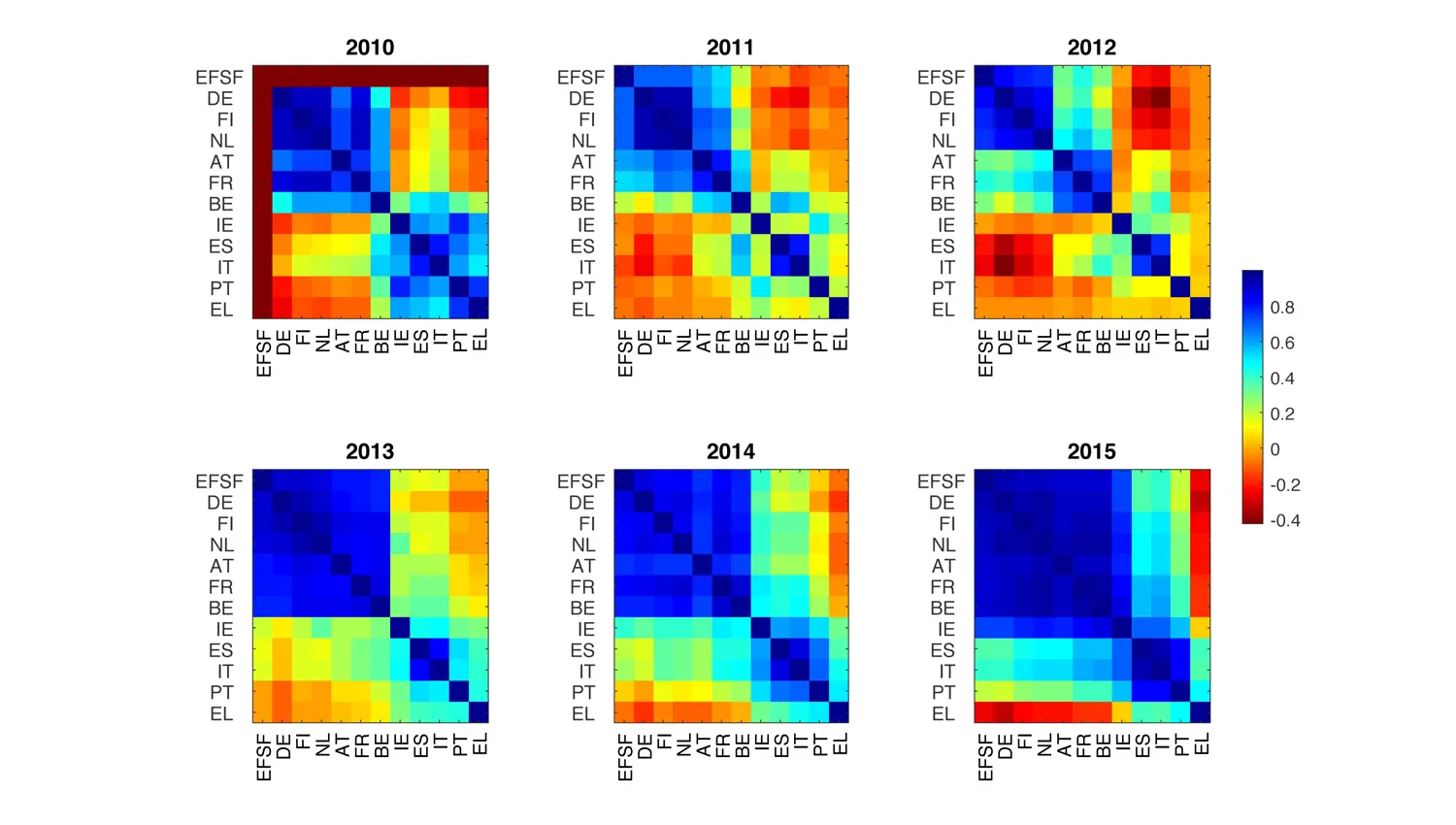

Description

From 2004 to 2015, the market perception of the sovereign risks of euro area government bonds experienced several different phases, reflected in a clear time structure of the correlation matrix between the yield changes. “Core” and “peripheral” bonds cluster in a bloc-like structure, but the correlations between the blocs are time-dependent and even become negative in periods of stress. Using noise-filtered partial correlation influences, this time-dependency can be evaluated and visualized using network graphs. Our results support the view that market-implied spillover risks have decreased since the European rescue and stability mechanisms came into force in 2011. EFSF bond issues have been trading as part of the “core” bloc since 2011. In 2015, spillover risks reappeared during the Eurogroup’s negotiations with Greece, although the periphery yields did not show risk spreads that were as large as those in 2012.

Key data

Projectlead

Prof. Dr. Peter Schwendner, Dr. Martin Hillebrand

Project team

Project partners

European Stability Mechanism ESM

Project status

completed, 09/2016 - 12/2018

Institute/Centre

Institute of Wealth and Asset Management (IWA); Institute of Computational Life Sciences (ICLS)

Funding partner

EU and other international programmes

Further documents and links

Publications

-

European government bond dynamics and stability policies : taming contagion risks

2016 Schüle, Martin; Schwendner, Peter

-

European government bond dynamics and stability policies : taming contagion risks

2015 Schwendner, Peter; Schüle, Martin; Ott, Thomas; Hillebrand, Martin

-

European government bond dynamics and stability policies : taming contagion risks

2015 Schwendner, Peter

-

Stress test scenario : eurozone meltdown

2015 Kelly, Scott; Chaplin, Andrew; Coburn, Andrew; Copic, Jennifer; Evan, Tamara; Neduv, Eugene; Ralph, Daniel; Ruffle, Simon; Schwendner, Peter; Skelton, Andrew; Yeo, Jaclyn Zhiyi

Gertrudstrasse 8

8400 Winterthur